Shrinking Supply with Buyers Getting Used to the Heat

Many of the same supply trends that we identified in our Spring Market Pulse remain in full effect as we get deeper into the Summer Market. The Mortgage Rate Lock-in effect has persisted with Sellers still largely preferring to sit on the sidelines versus give up their sub 4% rate to purchase a new home in the mid to upper 6% range. New listings in June were down 40% in the DC Metropolitan Area versus June of 2022 and active inventory in the region is now 50% lower than pre-pandemic inventory levels from 2019! There is now just 1.35 months of supply in the marketplace (a 6 month supply is considered a balanced market between Buyers and Sellers).

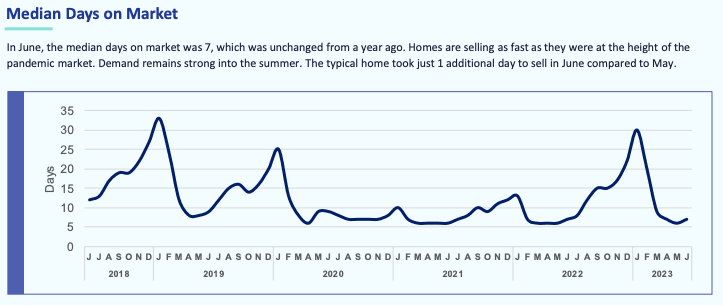

Buyer demand, on the other hand, has remained robust as Buyers have acclimated to the "new normal" rate environment. Overall property showings are down 10% YoY but with new listings down 40% that means the properties that do make it to the market are receiving more attention from Buyers that have been starved of options for far too long. The median days on market sits at just 7 days throughout the region which is equivalent to the pace of the feverish pandemic market but a sharp decline from this past Fall and Winter when days on market peaked at around 30 days. That high water mark in days on market corresponded with the lightning fast rise of interest rates from 5% to 7% in the second half of 2022. That rapid rate increase caused Buyers to pull back in large numbers leaving homes on the market to linger for far longer. Now with far fewer homes on the market and almost a full year of acclimation to the "new normal"- we should call it the "return to normal" as the average interest rate over the past 50 years is 8%- Buyers are back to competing for well priced properties that show well.

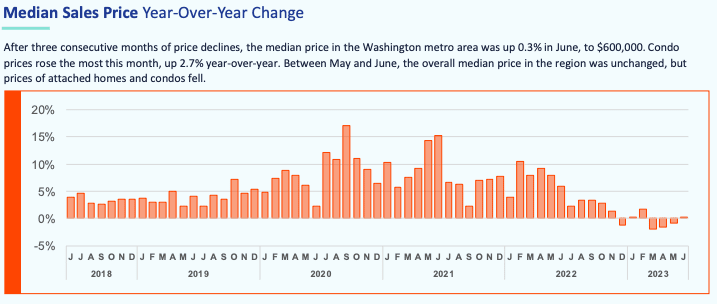

April Showers Bring a June Return to Price Appreciation

There was no way that this Spring was going to compete with last Spring from a price appreciation standpoint but if you consider that interests rates were around 3.75% in March of 2022 and 6.75% in March of 2023, the fact that prices only fell by 3-4% YoY during that time is remarkable on its face. As we have discussed, falling inventory was a large factor in keeping prices from falling further but the strength of our local economy also played a large part in continuing to support demand even with higher borrowing costs. With a less dramatic change in interests- June of 2022 saw rates in the mid-5's and June of 2023 saw rates in the mid-6's- combined with the dynamics highlighted above, this year's Summer Market is back to seeing YoY price gains in the region as a whole.

And Now We Predict the Future

The latest Consumer Price Index (CPI) data for June provided the best news on inflation in two years. The CPI rose only 3% YoY and only .2% compared with the month prior- beating economists' and Wall Street's expectations. Considering inflation was at 9.1% in June 2022 it is becoming clearer that the FED's policies have had their desired effects in many (but not all) respects. Housing costs still make up the lion's share of inflation accounting for over 70% of the June increase, but there are signs that rental rates are falling from pandemic highs and we will continue to see numbers improve on that front. Job growth is tapering and GDP growth is moderating yet June's consumer confidence index was the highest since January of 2022.

So it would largely appear that the FED's actions are having the desired effect of a softish landing in slowing the economy and taming inflation without sending the economy into a painful recession. Most analysts expect at least another .25% raise in the Fed Funds Rate this year, but are hopeful that we could be at the end of the interest rate hiking cycle by the end of this year.

If the tightening cycle ends in 2023 as we expect it will and interest rates begin to fall, we expect housing price appreciation to further accelerate as we will see an increase in Buyer demand without a significant enough increase in inventory to balance it out. Eventually, if rates come down far enough (into the low 5's), we should see the lock-in effect subside to some degree which will help with inventory levels. However, we will remain in an inventory shortage for the foreseeable future as the strength of our economy - with 75,000 jobs added to our local job market YoY in 2023- will continue to outstrip the growth of our housing stock.