2022 was a wild ride for real estate in the DMV.

While we did not experience the highest highs or the lowest lows that marked more volatile markets- particularly in the Southern and Western regions of the US- we still saw a feverish Spring Market followed by a very chilly Fall and Winter Market. Rapidly rising interest rates drove the market throughout the year with increased urgency fueling the Spring Market as rates rose sharply and Buyers did not want to miss out on the end of cheap money. Faced with limited inventory and tons of competition for homes, Buyers pushed prices to record highs. As rates continued to rise along with prices, many Buyers increasingly found themselves getting priced out of neighborhoods that they would have easily qualified for just six months earlier which led to a difficult decision to either downsize their ambitions, hit pause altogether on their plans to find a home in 2022 in hopes that rates or prices would come down in the near future, or forge ahead and increase their budgets to purchase with the expectation that they could refinance in the future.

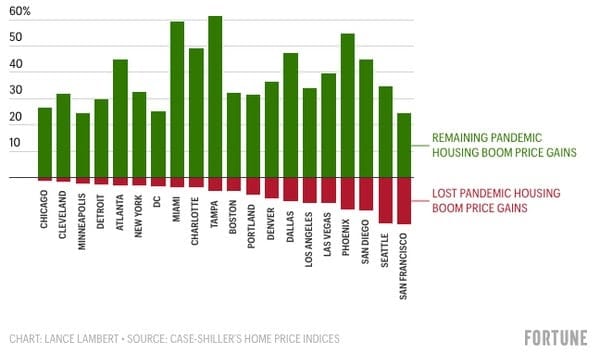

Unfortunately for those Buyers that chose to wait it out, many Sellers also decided to delay plans for selling their homes in the Fall and Winter which led to supply destruction that largely mirrored the drop in demand in our market. The result was a slight softening in prices from their June peaks but nowhere near the fall off that other markets experienced, especially the aforementioned markets whose significantly higher percentage of investors, PE speculators and iBuyers drove larger and far less sustainable pandemic price bubbles.

So Where Are We Now?

2022 ended on a positive, hopeful note after several months of encouraging economic data on inflation showed that perhaps the worst was over and that a Fed pivot could be in the cards early in 2023. Mortgage rates fell off their November highs and Buyers entered 2023 with a new sense of confidence - or at least the realization that prices weren't going to come crashing down as they had hoped - that was reflected in a significant uptick in mortgage application activity as well as showing and contract activity. This resurgence in activity is now being tested by another bump in interest rates following recent data that has shown that inflation in certain segments of the economy is proving incredibly sticky and a Fed pivot may still be quite a ways off.

The Lock-In Effect

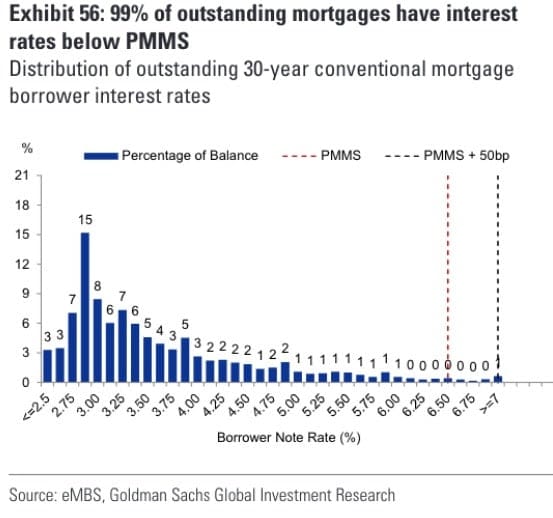

It remains to be seen how this latest rise in rates materially affects the demand side of the housing equation. What does seem clearer at this point is that supply will continue to be highly constrained until rates come down. After so many years of rock bottom rates, the vast majority of homeowners currently have a rate so favorable that selling and facing the prospect of buying at a considerably higher rate is a significant barrier to improving our inventory levels. 99% of homeowners have an interest rate below 6% and 70% of homeowners have a rate below 4%. This "lock-in effect" will likely continue to keep a high floor on prices.

Silver Linings for Sellers & Buyers

Due to the unique characteristics of the DMV market, with our relatively strong and stable local economy and relatively low percentage of investor/speculative purchases, our market enjoys a stability that few other parts of the country can match. Homeowners in our area have retained a large percentage of the home price appreciation they have experienced during the pandemic so even though prices may have peaked in the short term, Sellers putting their home on the market now will face less competition and still find a large enough pool of buyers to achieve great outcomes. Those who wait may find a more favorable rate environment in the future, but they are also likely to see considerably more "For Sale" signs in their neighborhood if that occurs.

For Buyers, while interest rate increases coupled with home prices that have retained most of their pandemic gains have certainly put a crunch on affordability, there has been some rebalancing of the power dynamic between Buyers and Sellers in their favor. While homes that are priced right and show well are still selling- often with competition- that competition is now somewhat constrained and escalations running hundreds of thousands of dollars above any reasonable measure of value are largely non-existent. Buyers can take some of the sting out of higher interest rates by taking advantage of lower priced adjustable rate mortgages and using strategies like mortgage rate buydowns. When rates do eventually adjust back down (and they will at least to some degree), Buyers who buy now at lower prices- often with contingencies in their contracts that were unheard of during the pandemic- and refinance later will capture more equity in the long run than those who continue to sit out a market that is still facing a systemic housing shortage and will almost certainly continue to appreciate to higher levels in the near future.