While the dynamics between supply, demand and price action in our housing market have been fascinating to watch in 2024 they have not always been kind to those on the wrong side of the pendulum swings in market sentiment between the various micro-markets of the DMV and across different property types. With all the various factors at play- rising and falling interest rates in response to signs of soft landings mixed with data showing the potential for a bumpier economic ride, dramatic changes in a Presidential race with very different public policy outcomes hanging in the balance and traditional seasonal forces buoying or exerting their gravity on markets it has been especially difficult this year to distinguish the signal from the noise.

Are showings down because we have had triple digit heat and an earlier start to the summer travel season than normal or has strained buyer affordability finally caused sentiment to turn? Are inventory and prices climbing along traditional seasonal patterns with a Spring Rise, a Summer Plateau and a gradual Winter Fall or will interest rates that are already at 15 month lows with a long awaited Fed cut finally in the works cause Buyers to jump back into the market en masse for a stronger than expected Fall and Winter Market? Are some of the more dramatic changes to our local markets spurred by the pandemic finally mitigating or becoming more entrenched as the new normal? These are just some of the questions that we have grappled with alongside our clients in 2024. By digging into the best data available (more on our new partnership with Altos Research to come) and leaning into our extensive personal network of the region's top agents to get the most comprehensive picture of the market, we have been able to achieve some extraordinary outcomes despite the market volatility.

The Ups and Downs of 2024: A Strong Start

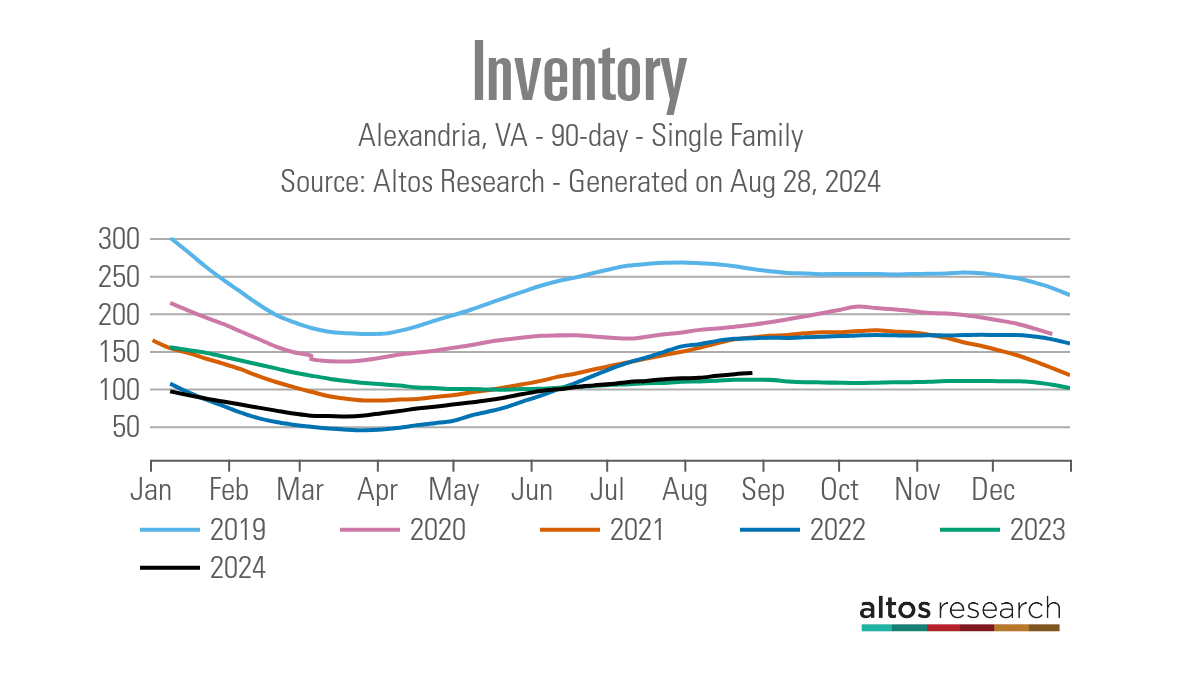

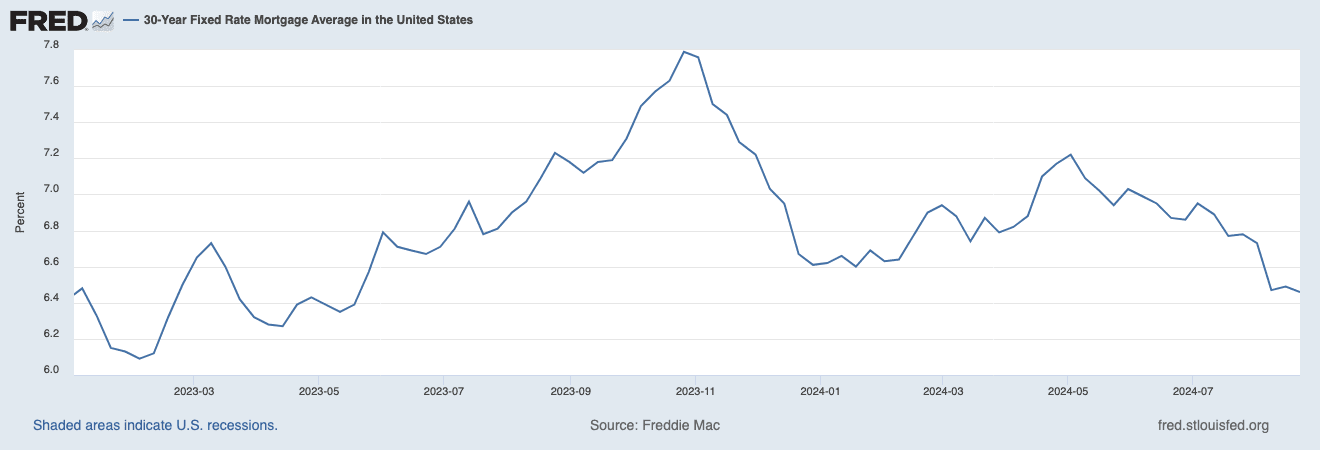

Inventory levels started the year below where they started 2023 in all the major DMV markets and interest rates fell almost a full percentage point from their Fall 2023 highs in the mid-7's to start the year in the mid-6's. This combination of low supply and increased affordability led to solid price appreciation early this Spring, particularly in the single family home market in Upper NW DC and the suburbs. Unfortunately, the expected rate cuts from the Fed did not materialize and interest rates rose for much of the Spring. At the same time, inventory was being added to the market thanks to our normal seasonal Spring increases creating headwinds in the marketplace.

A Tale of Two Markets: Downtown Versus the Suburbs

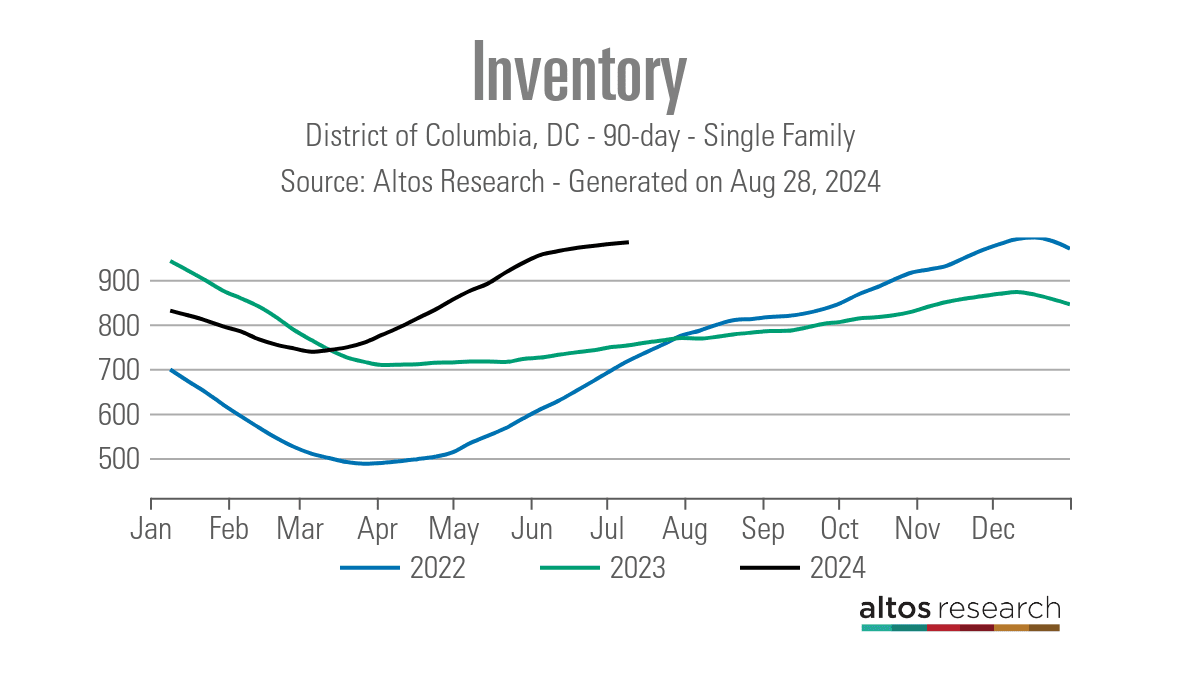

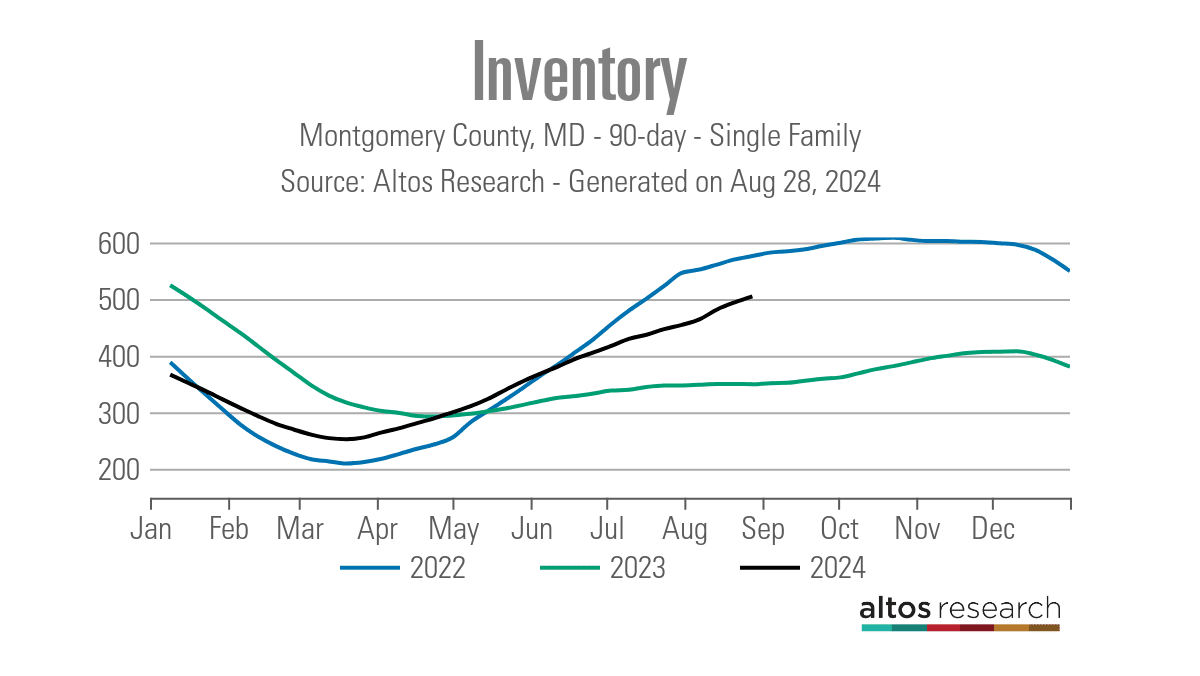

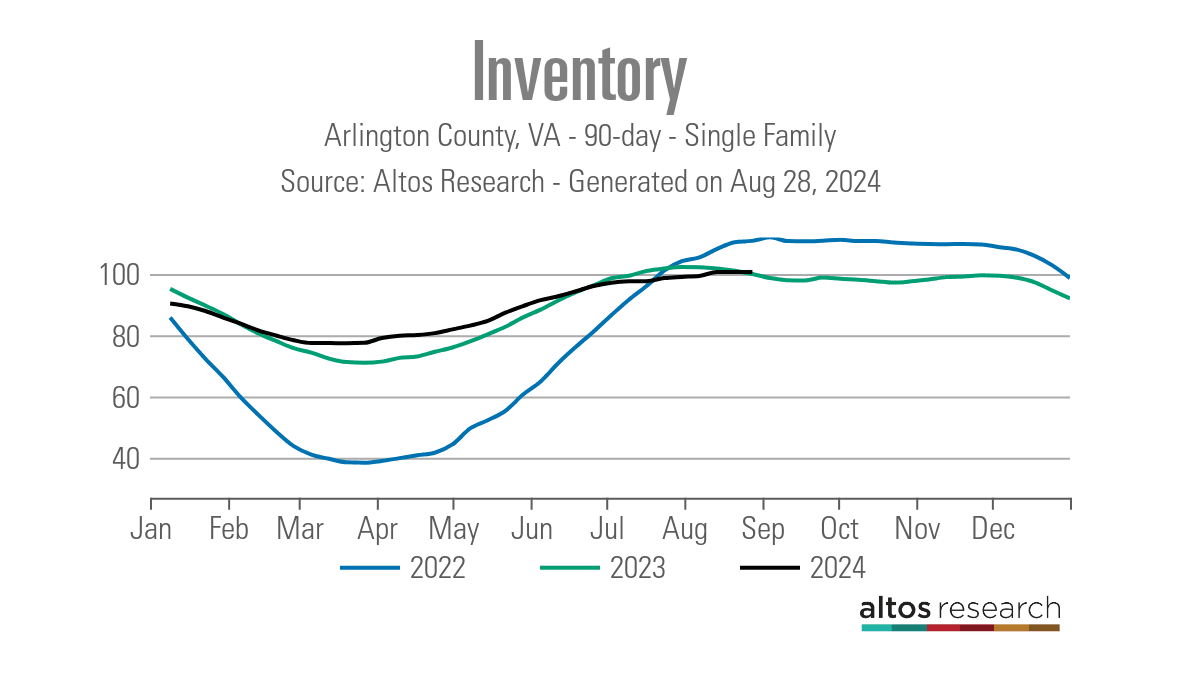

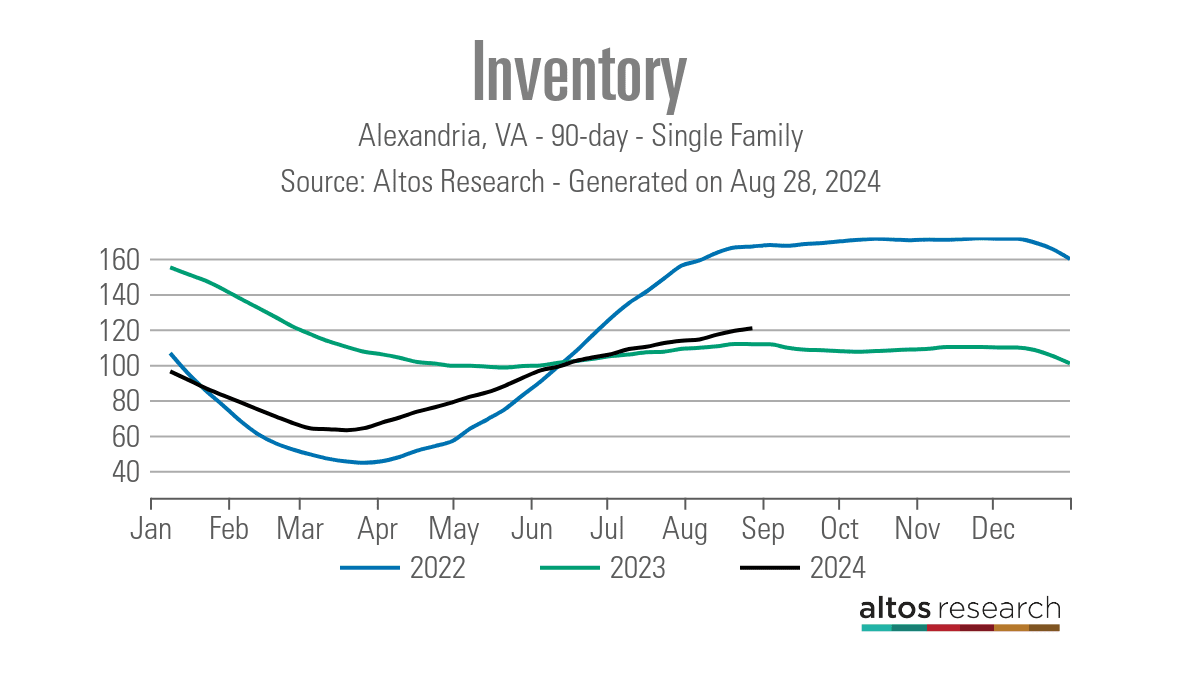

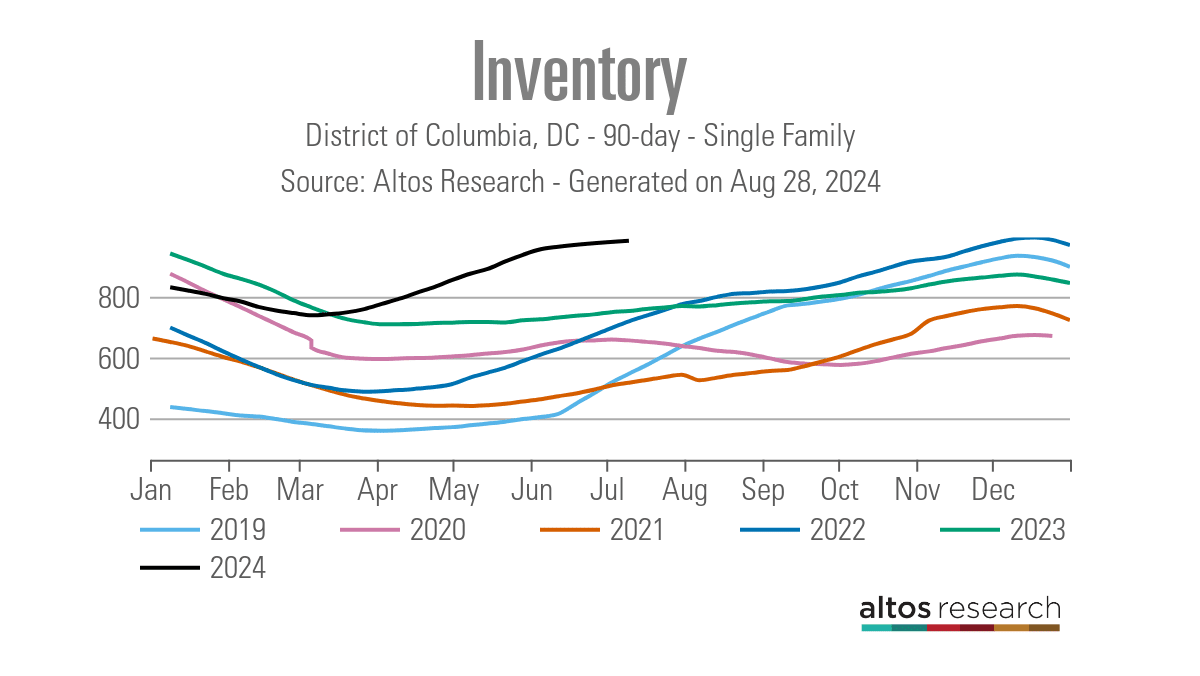

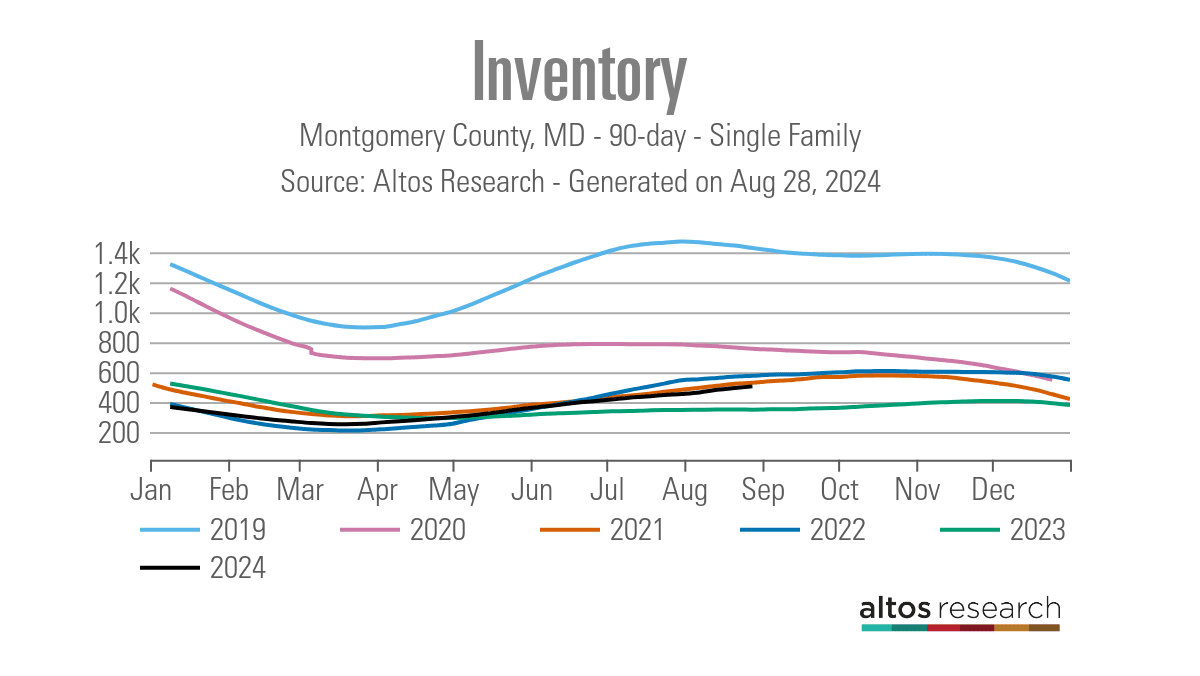

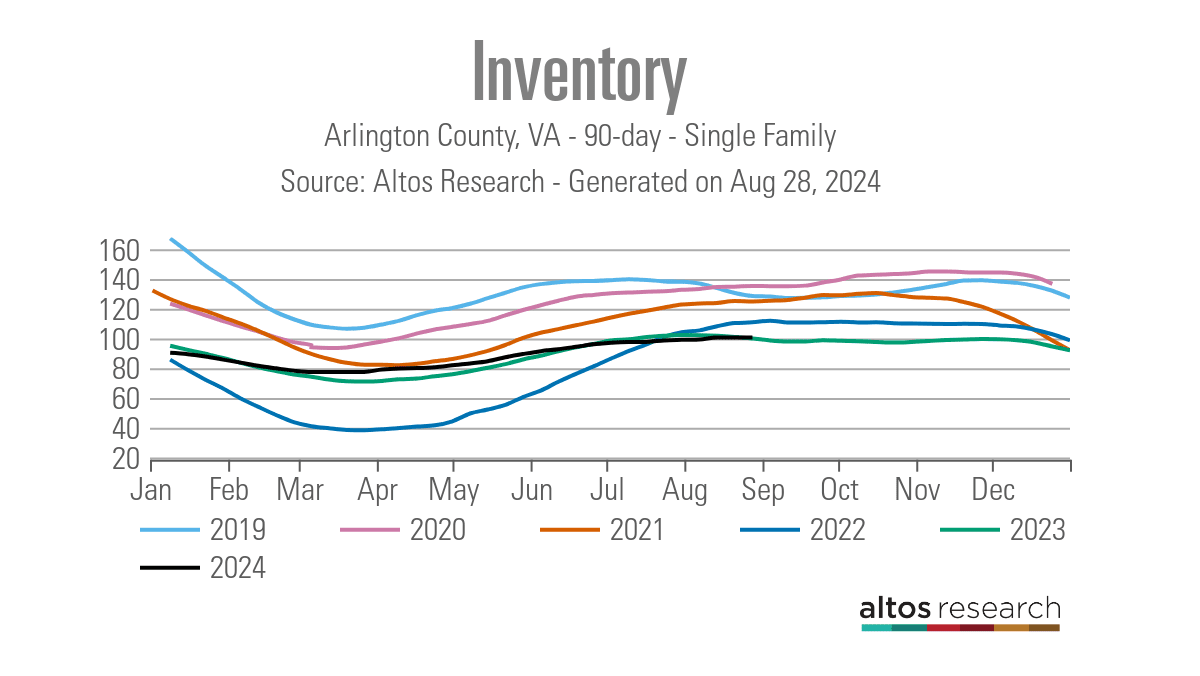

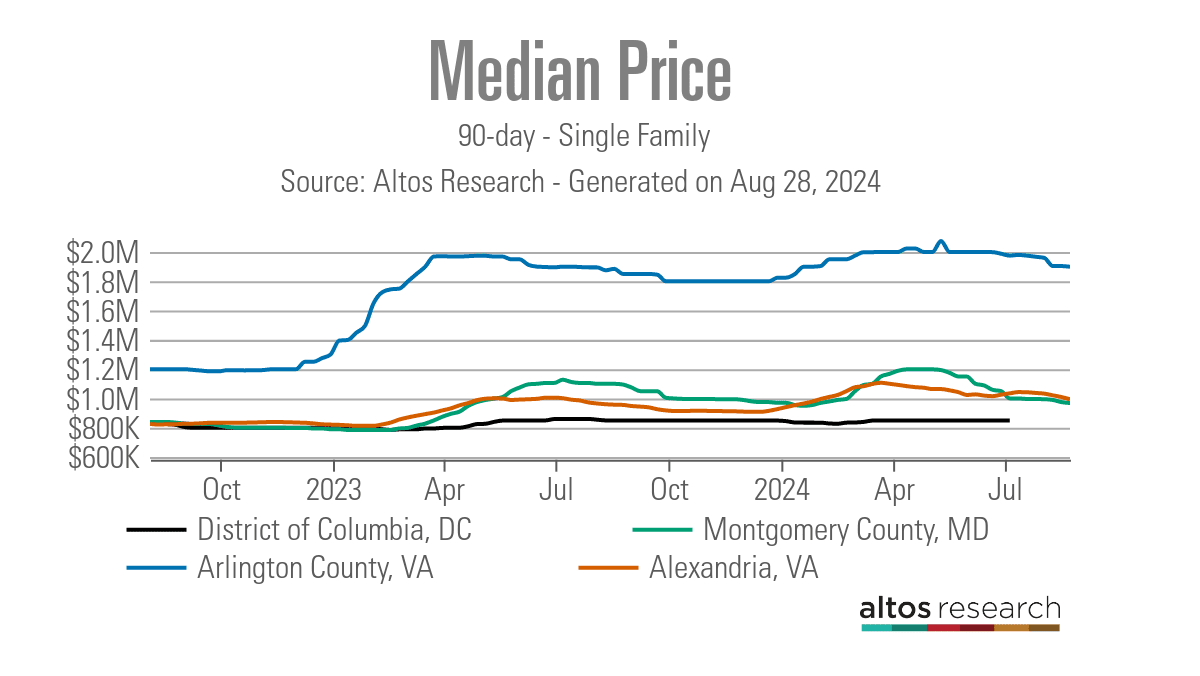

For the DC Market, inventory surpassed its 2023 levels in March while supply in the MD & VA suburbs remained below their 2023 levels until around June. This dynamic continued to widen the gap between the fortunes of DC sellers and their suburban counterparts. Eventually, increased prices from the early Spring Market and increasing interest rates continued to reduce affordability leading to a slowdown even in the suburbs as Summer started. Several weeks of records temperatures, an earlier and more active summer travel season than recent years, and a disastrous debate performace by Joe Biden which injected heightened uncertainty into our politics and our markets also weighed on demand in early Summer as inventory continued to rise. By mid year, we were experiencing elevated prices and inventory levels in Montgomery County versus 2023 and inventory levels in DC that were 34% higher than 2023. Northern Virginia, by contrast, saw its inventory more closely mirror Summer inventory levels from last year. We saw this softening firsthand with clients who were able to negotiate $100,000 off a fabulous new construction home in Bethesda before it hit the market...something that would have been unthinkable just three months prior.

In talking about increasing inventory, it is important to put these increases in context by jurisdiction when discussing how these changes exert different degrees of downward pressure on prices. While Montgomery County, Arlington and Alexandria have seen equivalent or slightly higher levels of single family inventory than last year, they are still far below pre-pandemic inventory levels and far below a balanced market. Prices in these markets are still rising at a good clip overall on a year over year basis. The District, on the other hand, is now seeing supply levels well above even pre-pandemic levels and is now considerably closer to the 6 months of inventory that is considered a balanced market than the close in suburbs. Pricing, though still rising, has flattened considerably in the District as a result.

A Mid Summer Rate Reversal

The economic numbers over the early summer months finally started to reflect what many in the business community had long been feeling but not yet seeing consistently in the data that the Fed relies on to inform its rate setting policies. With inflation continuing to come down and unemployment rates on the rise, the markets gained renewed confidence in a September rate cut and mortgage interest rates have been falling since late May and have now reached their lowest levels in 15 months.

The Tide is Finally Turning on Rates...Will Price Increases Follow?

Late Summer in the DMV is typically one of our slowest periods for activity in the real estate market so it is hard to fully gauge the effects of more attractive rates on Buyer demand right now. That being said, we are seeing increased Buyer activity that indicates that higher inventory, better rates and softening prices have brought some savvy Buyers back to the table to some degree. We anticipate a stable market this Fall as improving conditions for Buyers may be offset by some Buyers choosing to wait for even lower rates or until after the uncertainty around the November election clears to make their move. We believe that waiting will likely be to their detriment- particularly for those buyers looking in the suburbs- as we expect prices to accelerate at a more robust pace in 2025 as further rate cuts will unleash significant pent up Buyer demand before rates get low enough to unlock enough inventory to meet that demand.

If rates fall below 6% in 2025 -both Fannie Mae and the Mortgage Bankers Association are currently predicting rates to fall to 5.9% by the end of 2025- that will likely spur more Buyers to enter or return to the market to take advantage of rates that would be back at 2022 levels. Sellers, on the other hand, will likely need rates to fall significantly further- considering 60% of homeowners have an interest rate below 4%- before they return to the market in numbers great enough to relieve inventory pressures. So unless there is considerable demand destruction, the inventory shortage that we face, particularly in the suburbs, should continue to exert upward pressure on prices. The District's fortunes are certainly murkier but could also improve considerably if urban revitalization efforts succeed (thank goodness for the Wizards & the Caps staying in town), progress on crime (which has significantly improved in 2024) continues and the huge millenial generation aging into their peak home buying years drives increased demand back to the urban core.