There has been a lot of misinformation about the DC Metropolitan Area real estate market that has been making the rounds on social media of late. So, in an effort to bring a small bit of sanity and reason back to the one aspect of your lives that we feel uniquely suited to comment on, we want to provide you with some facts about the current state of the real estate market. We also want to give you a sense of the various factors- many of which remain to be determined- that could impact valuations in our marketplace moving forward.

Let us start by recognizing the devastating personal impact to so many of our friends, family, neighbors, communities, institutions and values. In our combined 30 years in real estate (and 80+ years living in the DC area), one of the greatest joys of our professional and personal lives has been getting to work with and learn from a broad swath of incredible clients from all walks of life- many of whom we consider like family. If we can tap our network to assist anyone who needs a connection during these times, we are beyond happy to do so. Ok, back to real estate...

Inventory is Not Spiking Due to Federal Layoffs and Prices are Not Spiraling in Our Region

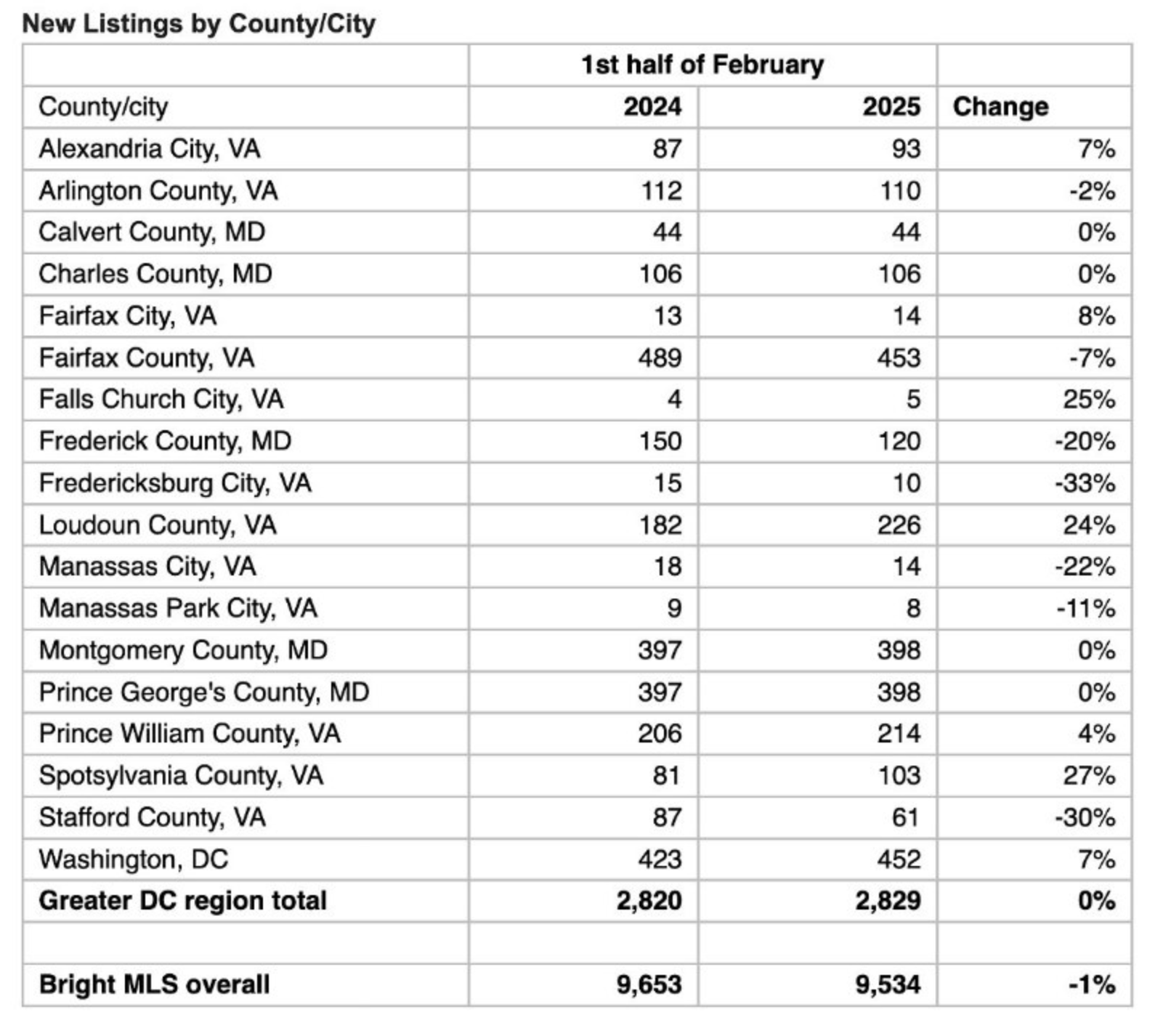

Some recent viral social media posts have claimed that a flood of new inventory has hit the market as Federal employees are losing their jobs and rushing to sell their homes. While there is no doubt that a portion of our local workforce- note that 85% of the federal workforce lives outside the DC Metropolitan area- has been affected by recent events, data from the first two weeks of February show virtually no change in levels of "active" and "coming soon" inventory in most sub-markets in our region compared to the same period from last year.

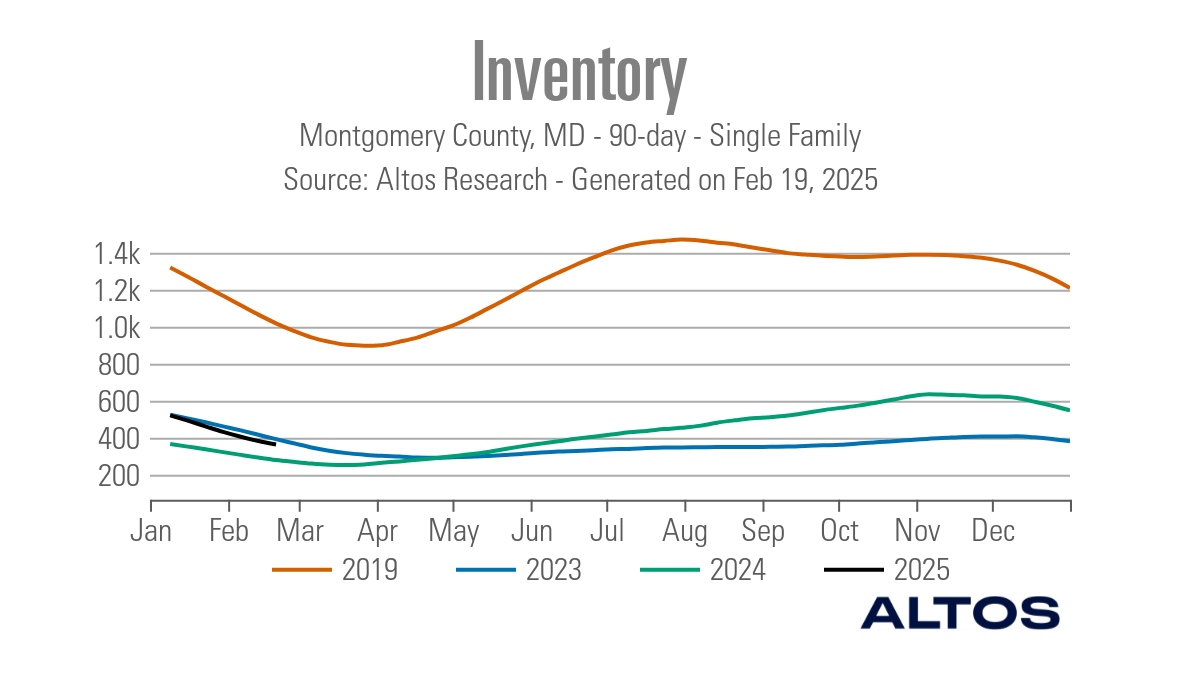

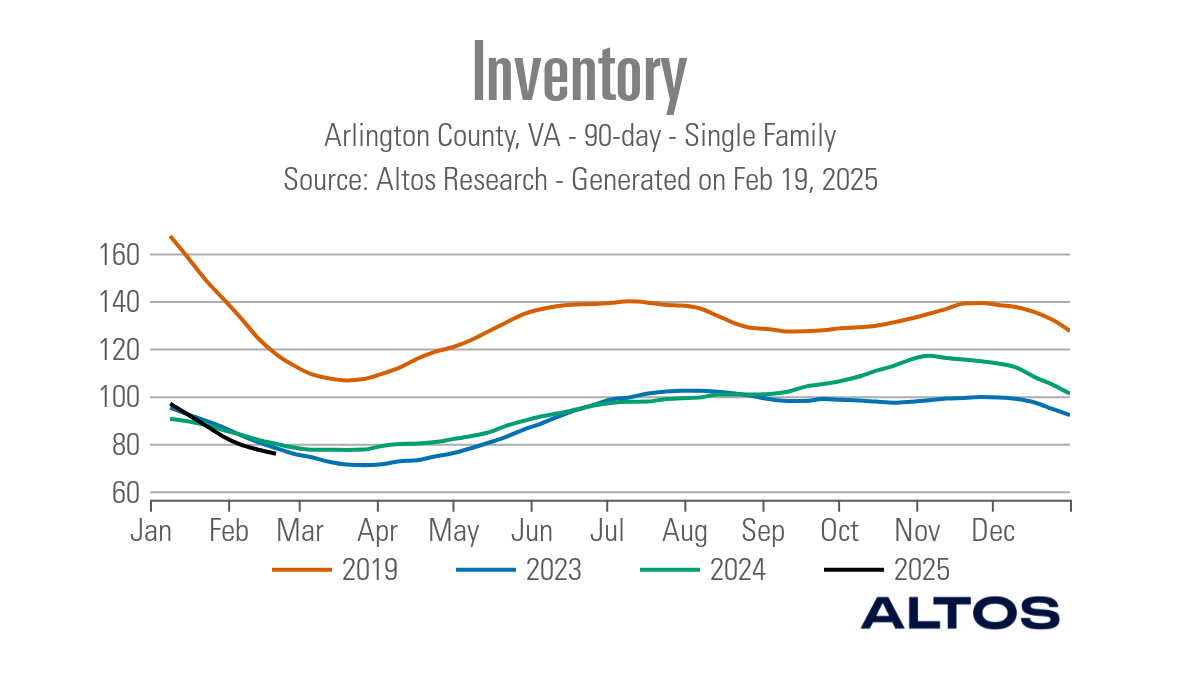

Notably, the District is seeing an increase in inventory of 7% YoY for this time period. However, inventory levels are slightly below where they were at this time in February of 2023 and consistent with the elevated inventory trends that started during the pandemic and have persisted over the past four years. Whereas DC's inventory is well above pre-pandemic levels, Arlington County and Montgomery County continue to see inventory levels well below pre-pandemic levels.

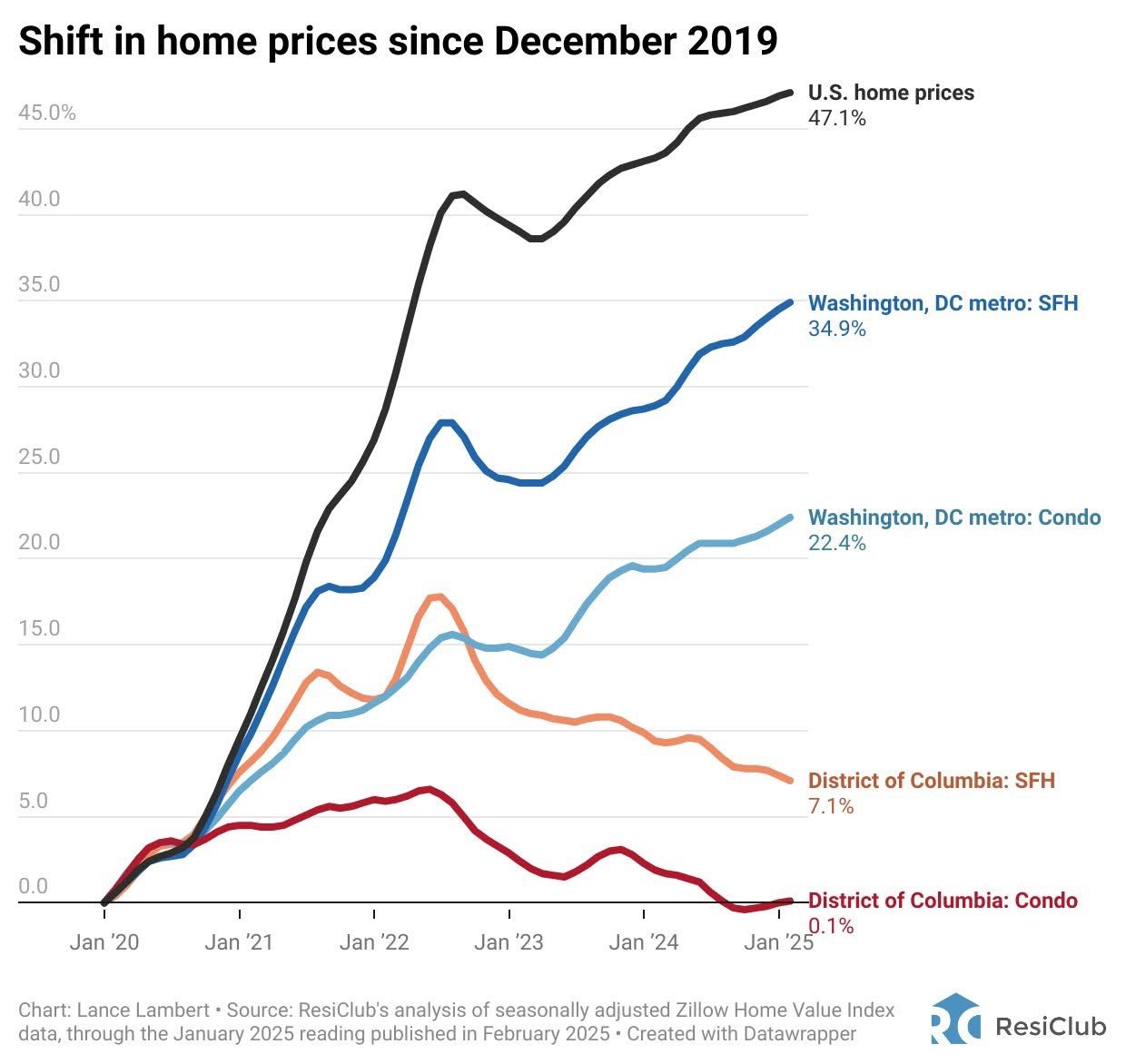

From a pricing standpoint, we are continuing to see a growing separation between pricing appreciation in the single family home market in the close-in suburbs- which have been booming since Covid and continue to be severely inventory constrained- and the single family home market in the District- which has been more affected by interest rates that have been above 6% for nearly two and a half years. Even with the softness that the District has seen overall compared to the suburbs, median home prices are still up 6-7% since the start of Covid for single family homes and those numbers vary significantly based on individual zipcodes.

Condos in the District have continued to lag all other property types with almost no appreciation since the start of the pandemic due to a perfect storm of external and internal factors. The initial Covid shift away from condo living dealt the first blow, followed by a shift to remote work and concerns about crime that pushed many to the suburbs and exurbs (these two factors affected single family homes in the District as well). Finally, higher interest rates starting in 2022- which disproportionately affect younger buyers and first time homebuyers- have led to further softening for condo values. Return to work mandates and a sharp decline in the rate of violent crime in the District since 2024 (down 35% since 2023) are two factors that should contribute to better prospects in the future if employment prospects do not deteriorate significantly and interest rates improve over time.

Short Term and Longer Term Trends to Follow

While the viral videos and many of the headlines are not accurate, there is no denying that we are experiencing significant disruption and uncertainty injected into our local economy and there is no doubt in my mind that it will have an effect on our real estate market as we head into the Spring Market. The question is to what degree, over what time period and whether or not some factors will counterbalance each other to mitigate the overall impact on home valuations in our area. Generally speaking, while I believe there will be an impact, I do not foresee anything approaching some of the alarmist predictions that have gained traction online thanks more to ideology than to accuracy and reason. Here are some of the factors that we will be watching as the Spring Market takes shape to see how they affect the overall housing market moving forward:

Legal Challenges and Constituent Pressure

What percentage of the administration's desired plans to further cut the federal workforce will be held up or blocked by the courts? Will injunctions against federal funding freezes ultimately be successful at slowing down or stopping these executive actions? Will mounting pressure from constituents affected by actual or proposed funding cuts have any impact on the pace and severity of proposed cuts? I have my doubts about the courts ability or appetite to engage, but I could certainly see a world where falling approval numbers, an significant uptick in unemployment or a correction in the stock market leads to increasing pushback behind the scenes.

Finding New Employment in the Region

How many federal employees will be able to transfer their skills to the private sector which has continued to grow throughout our region? Given the fact that the vast majority of homeowners have mortgage interest rates in the 3-4% range there are still strong incentives to stay in place and the federal workforce is both highly skilled and highly educated which increases the likelihood that federal employees will be able to pivot to other industries in our region. Those calling this DC's steel mill closure moment on social media ignore the fact that highly skilled workers in a diversified economy have far more mobility than blue collar workers in a town that loses its only source of employment.

Return to Work Policies

The proliferation of remote work during the pandemic was the biggest factor in dramatically shifting housing demand in our area with the suburbs and exurbs seeing huge increases in demand from Buyers who no longer needed to factor commute times or proximity to public transportation into their purchase calculus. Now that the pendulum on remote work is swinging sharply back towards a return to office in both the private and public sector we should see demand return to the urban core, closer-in suburbs and Metro accessible neighborhoods (Metro recorded its highest ridership numbers since 2020 in early February). This process will likely take longer to unfold than it did between 2020-2022 when interest rates were lower resulting in less financial friction in moving but it will still be a trend to watch moving forward.

Timing Effects & Absorption Rates

Even for those who do lose their jobs and for whatever reason decide to leave the DC Metropolitan area, selling ones home takes time and planning. Homes do not just flood the market, especially in a marketplace where the investor ratio is far below the national average (DC had only 11% investor sales in Q2024 versus a national average of 18%). Furthermore, particularly in the suburbs, we have been at such a low inventory environment for so long that the market could absorb a fair amount of additional inventory without it affecting prices dramatically. Montgomery County, MD currently has only a one month supply of homes while Arlington County has only 1.3 months of supply. Historically, six months of inventory indicates a balanced market. Overall, the District has 3.9 months of inventory and the District's condo market sits at 4.9 months of inventory so it is more susceptible to tipping into a Buyer's Market. That being said, even with rising inventory, the median price in 2024 for all homes in DC rose 4.5% YoY.

A Pivotal Spring Market Awaits

The bottom line is that with 15% of the approximately 2.3 million person civilian Federal workforce living in the greater metropolitan area and with up to 40% of our overall local economy tied to federal spending, targeted reductions to the federal government will disproportionately affect our region and exert downward pressure on our housing market. That being said, there are a variety of factors that could mitigate the ill effects of an increase in inventory and a potential softening of demand. Moreover, these effects will not be felt equally across the region based on the varying degrees of slack in the market amongst different property types and different sub-markets within our regional housing market. Our region has been remarkably resilient in the past and continues to face a longer term structural shortage of housing. With a highly skilled and highly educated workforce as well as a far more diversified economy than in decades past, there are a lot of reasons to believe that our market will be able to weather the storm.

The coming Spring Market, where both prices and inventory tend to rise to their highest levels of the year, will be our first real look at where buyer demand is after a chilly Winter and even chillier politics contributed to a rather sluggish January and February Market.